When Mr. Saeed started his trading business in the UAE, everything felt simple. A few invoices, basic expense tracking, and occasional bank statements were enough to run things smoothly. There was no pressure, no fear of strict compliance, and no serious worry about detailed accounting. Life was easy — until Corporate Tax officially entered the system.

At first, Mr. Saeed thought it was just another government announcement that wouldn’t really affect small businesses like his. He heard words like Corporate Tax Law – Closing Provisions, UAE Corporate Tax – Transitional Rules, and Tax Registration and Deregistration, but they sounded more like legal jargon than real-life business problems.

The First Reality Check

One day, Mr. Saeed received an email reminding him to ensure his business was properly registered under the new tax system. That was the first time he seriously looked into Tax Registration and Deregistration and realized something shocking: without proper financial records, even registration becomes complicated.

He had no structured profit and loss reports, no clear record of adjusted expenses, and no accurate balance sheet. Everything was scattered across WhatsApp invoices, Excel files, and handwritten notes.

Where the Real Problem Started

As time passed, his bank asked for audited financial statements. His supplier asked for verified financial proof to extend credit. At the same time, he started hearing from other business owners that the UAE Corporate Tax – Transitional Rules were not just “guidelines” — they were a serious part of how companies would be reviewed when moving into the new tax era.

These Transitional Rules meant businesses couldn’t just start fresh. They had to show how their numbers moved from the old system (when there was no tax) into the new corporate tax environment. And without proper accounts, that bridge simply couldn’t be built.

Mr. Saeed realized that he was sitting on a ticking time bomb.

The Fear of the Unknown

What scared him the most was learning about the Corporate Tax Law – Closing Provisions. He learned that under these provisions, the Tax Authority has full rights to ask for years of financial data, conduct audits, and impose penalties if the records are not accurate.

This wasn’t just about filing a return. This was about proving every number, every transaction, and every claim. At that moment, Mr. Saeed understood that accounts were no longer just a “business tool.” They had become a legal shield.

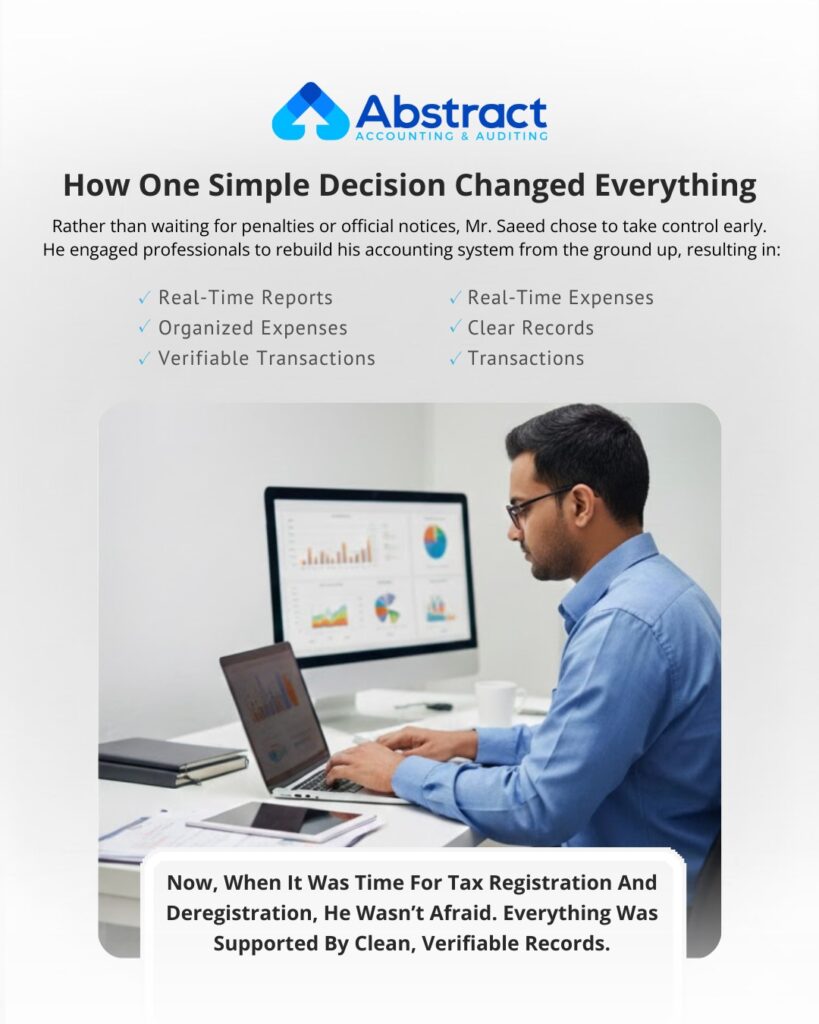

How One Simple Decision Changed Everything

Instead of waiting for a penalty or a notice, Mr. Saeed decided to fix the problem before it became unmanageable. He hired professionals to rebuild his accounting system from scratch.

For the first time, he saw:

- Real-time profit and loss reports

- Structured expense tracking

- Clear asset and liability records

- Organized invoices and bank reconciliations

Now, when it was time for Tax Registration and Deregistration, he wasn’t afraid. Everything was supported by clean, verifiable records.

A Lesson Many Businesses Are Still Learning

Mr. Saeed’s story is not unique. Thousands of UAE businesses are now realizing that the corporate tax era has completely changed how companies must operate.

The UAE Corporate Tax – Transitional Rules were designed to make the shift smoother, but only for those who prepared early. For those who ignored accounting, the transition has become painful, stressful, and expensive.

And the Corporate Tax Law – Closing Provisions make one thing very clear: the responsibility lies completely with the business owner.

- If your records are weak, the risk is yours.

- If your reports are wrong, the penalties are yours.

- If your audit fails, the consequences are yours.

The Reality Today

Today, Mr. Saeed’s business runs with confidence. He no longer fears emails from authorities. He no longer panics when someone asks for audited financials. He knows that his accounts are clean, compliant, and ready for any inspection.

And the truth is simple:

Maintaining proper accounts in the UAE is no longer optional. It is no longer a “good practice.” It is now a core legal requirement.

Whether it is complying with the UAE Corporate Tax – Transitional Rules, understanding the Corporate Tax Law – Closing Provisions, or managing smooth Tax Registration and Deregistration, everything connects back to one foundation — proper accounting.

How Proper Accounting Changed Everything for Mr. Saeed

When Mr. Saeed finally completed his first proper audit under the new corporate tax system, he expected stress. What he didn’t expect was the truth.

For the first time in years, his business was examined on a true and fair basis. The numbers were no longer based on guesswork or assumptions they were supported by real documents, real systems, and independent verification. During the audit, something shocking came to light.

Mr. Saeed discovered that a senior manager, who had been working with him for years, was quietly committing fraud. Small amounts here and there, fake supplier invoices, and manipulated expense entries things that were invisible without a detailed audit.

If it wasn’t for the structure created by Corporate Tax and the involvement of a professional audit firm, this fraud could have continued for years.

But instead of feeling broken, Mr. Saeed felt relieved. Because along with uncovering the fraud, the audit also revealed something positive his business was actually performing better than he ever imagined. He wasn’t just surviving. He was in real profit.

The Bigger Picture No One Talks About

Mr. Saeed began to understand the hidden reality behind the Corporate Tax system. This wasn’t just about collecting tax.

Because of the new laws, audit firms became more active and alert. Their technical knowledge started being used in real business environments. Skilled accountants, auditors, and tax experts started playing a stronger role in helping businesses grow, not just comply.

He noticed how:

- Financial transparency increased

- Professional standards improved

- Real expertise started getting valued in the market

- Businesses became more disciplined

- Hidden frauds started getting exposed

- Proper use of technical and financial skills increased

- Real business performance started showing in official numbers

- Investor confidence improved

- Banks and financial institutions gained more trust in UAE businesses.

- This wasn’t just helping him it was helping the economy.

Final Thought

Mr. Saeed’s biggest lesson was simple:

- Corporate Tax didn’t harm his business.

- Audit didn’t slow him down.

- Compliance didn’t weaken him.

- They made him stronger.

- And today he knows that:

- The system has changed.

- The law has changed.

- The expectations have changed.

If you don’t change with it, the system won’t wait for you.

Because in today’s UAE business environment, accounts are not just numbers — they are your legal protection.